Exploring the realm of Second Charge Mortgage Rates: What to Expect in 2026, this introduction sets the stage for an enlightening discussion that will captivate readers with its insightful and engaging narrative.

Further details on the topic will be provided in subsequent paragraphs.

Overview of Second Charge Mortgages

A second charge mortgage, also known as a secured loan, is a type of loan that allows homeowners to borrow money using the equity in their property as security. This means that if you fail to repay the loan, the lender can repossess your home to recover the debt.

Differences between First Charge and Second Charge Mortgages

First charge mortgages are the primary loans taken out when purchasing a property, while second charge mortgages are additional loans taken out on top of the existing mortgage. First charge mortgages have priority over second charge mortgages in terms of repayment if the property is sold.

Typical Uses of Second Charge Mortgages

- Home improvements: Many homeowners use second charge mortgages to fund renovations or extensions on their property.

- Debt consolidation: Some people consolidate their debts by taking out a second charge mortgage to pay off high-interest debts.

- Business purposes: Second charge mortgages can also be used to fund business initiatives or investments.

Factors Influencing Second Charge Mortgage Rates

When considering second charge mortgage rates, it's essential to take into account various factors that can influence the final rate offered to borrowers. These factors play a crucial role in determining the overall cost of borrowing through a second charge mortgage.Economic Conditions

Economic conditions have a significant impact on second charge mortgage rates. In times of economic stability and growth, interest rates tend to be lower, making borrowing more affordable. Conversely, during economic downturns or periods of uncertainty, interest rates may rise, leading to higher second charge mortgage rates.Credit Scores and Loan-to-Value Ratios

Credit scores and loan-to-value (LTV) ratios are also key factors that influence second charge mortgage rates. Borrowers with higher credit scores are generally seen as less risky by lenders and may qualify for lower interest rates. Additionally, the LTV ratio, which compares the loan amount to the value of the property, can impact the rate offered. A lower LTV ratio typically results in more favorable rates, as it signifies less risk for the lender.Trends in Second Charge Mortgage Rates

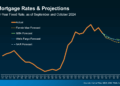

In examining the trends in second charge mortgage rates, it is essential to look at historical data to understand how these rates have fluctuated over time and what factors have influenced these changes. By comparing rates over the past few years, we can identify any patterns that may indicate how rates could evolve leading up to 2026 based on current trends.

In examining the trends in second charge mortgage rates, it is essential to look at historical data to understand how these rates have fluctuated over time and what factors have influenced these changes. By comparing rates over the past few years, we can identify any patterns that may indicate how rates could evolve leading up to 2026 based on current trends.Historical Trends

When we analyze historical trends in second charge mortgage rates, we see that these rates have varied significantly over the years. Factors such as economic conditions, lender competition, and regulatory changes have all played a role in shaping these rates. It is crucial to consider how these external factors have impacted the rates to make informed predictions about the future.- During periods of economic growth, second charge mortgage rates tend to decrease as lenders compete for business and borrowers have more options.

- Conversely, during economic downturns, rates may rise as lenders tighten their lending criteria and borrowers face higher costs.

- Regulatory changes, such as new lending rules or increased oversight, can also affect second charge mortgage rates by altering the risk profile for lenders.

Comparison and Analysis

By comparing the rates over the past few years, we can identify trends that may indicate how rates will evolve leading up to 2026. For example, if rates have been steadily increasing due to economic factors, it is likely that this trend will continue unless there are significant changes in the market. Analyzing these patterns can help borrowers and lenders make informed decisions about when to take out a second charge mortgage.It is important to monitor economic indicators, lender behavior, and regulatory changes to understand how second charge mortgage rates may change in the future.

Impact of Market Conditions on Second Charge Mortgage Rates

Market conditions play a significant role in determining second charge mortgage rates. Factors such as inflation, interest rates, and geopolitical events can all influence these rates, leading to fluctuations in the market. Understanding how these conditions impact second charge mortgage rates is crucial for borrowers and lenders alike.Inflation and Interest Rates

Inflation and interest rates have a direct impact on second charge mortgage rates. When inflation rises, central banks may increase interest rates to curb inflation. This, in turn, can lead to higher second charge mortgage rates as lenders adjust their rates to compensate for the increased cost of borrowing. On the other hand, if inflation is low and interest rates are stable or decreasing, borrowers may benefit from lower second charge mortgage rates.Geopolitical Events

Geopolitical events such as wars, trade disputes, or political instability can also influence second charge mortgage rates. These events can create uncertainty in the market, leading to fluctuations in interest rates. For example, a geopolitical crisis may cause investors to seek safer assets, resulting in lower demand for riskier investments like second charge mortgages. This decreased demand can push interest rates higher for these types of loans.Examples of Market Fluctuations

Historically, market fluctuations have had a significant impact on second charge mortgage rates. For instance, during the 2008 financial crisis, interest rates plummeted as central banks implemented measures to stimulate the economy. This led to a decrease in second charge mortgage rates, making borrowing more affordable for homeowners. Conversely, during periods of economic growth, interest rates may rise, causing second charge mortgage rates to increase as well.Comparison of Second Charge Mortgage Rates Across Lenders

When looking at second charge mortgage rates across different lenders, it's important to consider the variations in offers that can exist. Lenders may have different criteria, terms, and conditions that can impact the rates they offer to borrowers. This comparison can help borrowers find the best rates available to them.

When looking at second charge mortgage rates across different lenders, it's important to consider the variations in offers that can exist. Lenders may have different criteria, terms, and conditions that can impact the rates they offer to borrowers. This comparison can help borrowers find the best rates available to them.Variability in Loan Terms and Conditions

- Each lender may have specific eligibility criteria that borrowers need to meet in order to qualify for a second charge mortgage.

- The loan-to-value ratio, credit score requirements, and income verification process can vary between lenders, influencing the rates they offer.

- Lenders may also have different repayment terms, such as fixed or variable interest rates, which can affect the overall cost of the loan.

Finding the Best Rates

- By comparing offers from multiple lenders, borrowers can get a better understanding of the rates available to them.

- Using online comparison tools or working with a mortgage broker can help borrowers explore different options and find the most competitive rates.

- Borrowers should pay attention to not only the interest rates but also any fees or additional charges associated with the loan to get a complete picture of the cost.

Regulatory Changes Affecting Second Charge Mortgage Rates

As regulatory changes play a crucial role in shaping the lending landscape, it's essential to understand how these changes can impact second charge mortgage rates. These alterations can affect the overall cost of borrowing for consumers and influence the competitiveness of rates offered by different lenders.

Impact of Recent Regulatory Changes

Recent regulatory changes, such as updates to affordability assessments or modifications in capital requirements for lenders, can have a direct impact on second charge mortgage rates. Lenders may adjust their rates to comply with new regulations, which can lead to changes in the interest rates offered to borrowers.

Staying Informed as a Borrower

- Monitor official announcements: Keep track of any updates or announcements from regulatory bodies, such as the Financial Conduct Authority (FCA), regarding changes in regulations that may affect mortgage rates.

- Consult with lenders: Reach out to your lender to inquire about any upcoming regulatory changes and how they may impact your current or future mortgage rates.

- Work with a mortgage advisor: Seeking guidance from a mortgage advisor can help you stay informed about regulatory changes and understand their implications on second charge mortgage rates.

Conclusion

In conclusion, this deep dive into Second Charge Mortgage Rates: What to Expect in 2026 offers a comprehensive look at the subject matter, leaving readers with a clear understanding and valuable insights to ponder.

Essential FAQs

What factors influence second charge mortgage rates?

Factors include economic conditions, credit scores, and loan-to-value ratios.

How do second charge mortgage rates vary across lenders?

Rates offered by lenders can differ, along with varying loan terms and conditions.

What are the uses of second charge mortgages?

Second charge mortgages are typically used for home improvements, debt consolidation, or funding large purchases.

How can borrowers find the best rates for second charge mortgages?

Borrowers can compare offers from different lenders to find the most favorable rates.

{kind=link}